Analysis of 2024 venture investments. It’s all AI these days.

The Rightstack Research DB

From AI’s banner year to an 8-year low in global dealmaking, we break down key changes in the venture landscape using CB Insights data.

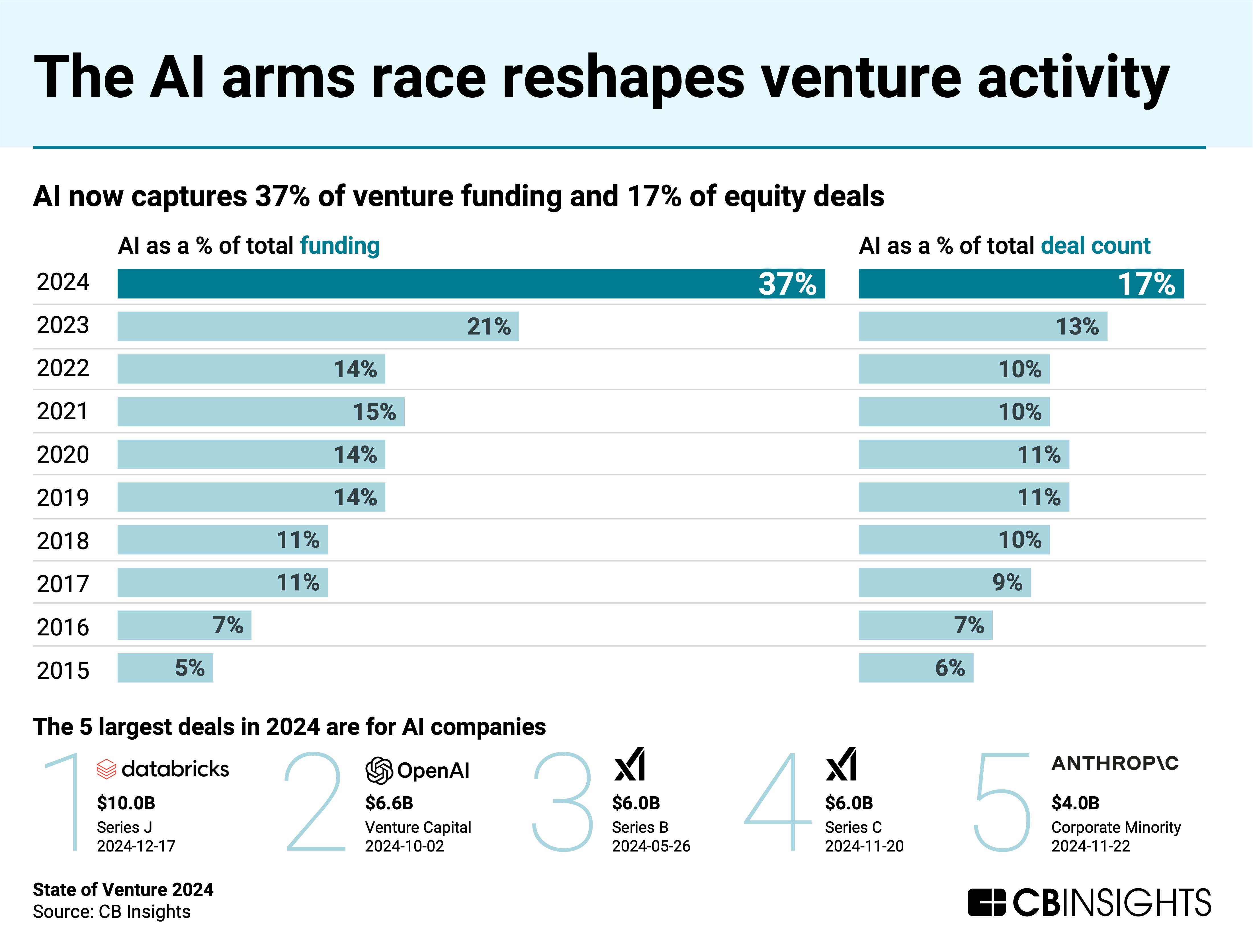

AI has reshaped the venture landscape, capturing a record share of funding (37%) and deals (17%) in 2024, including 5 of the year’s largest deals.

The AI arms race reshapes venture activity, capturing 37% of funding and 17% of deals in 2024

{kind=link}

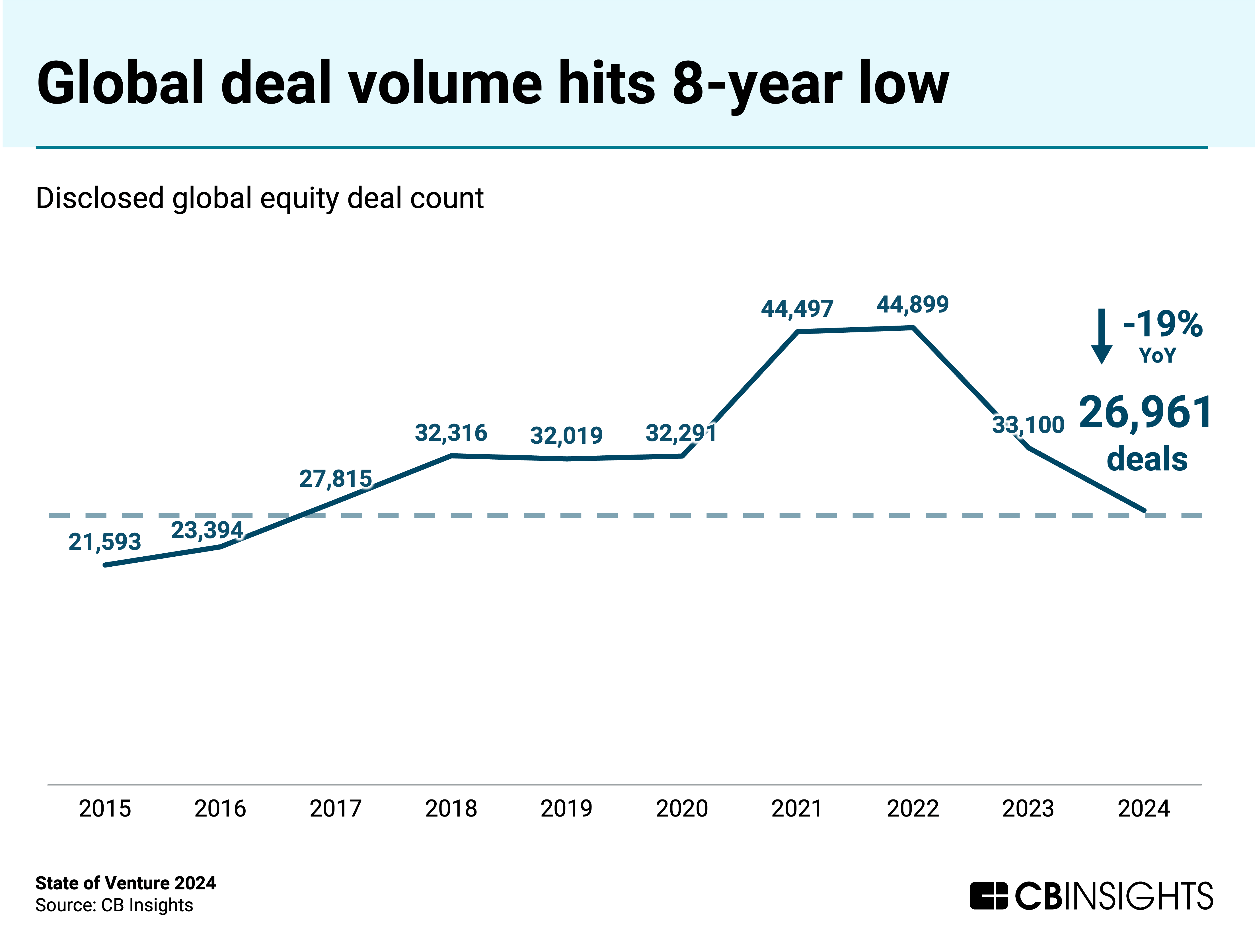

But beyond the momentum building in AI, global deal activity plunged 19% YoY to its lowest level since 2016, creating both challenges and opportunities for investors and corporate strategists.

Download the full report to access comprehensive data and charts on the evolving state of venture across sectors, geographies, and more.

Key takeaways from the report include:

AI is eating VC. In 2024, AI represented 37% of venture funding and 17% of deals — both all-time highs. AI infrastructure players raised all of the top 5 venture deals of the year, with 4 closing in Q4’24 alone — driving a 2-year high in quarterly funding. With nearly 3 in 4 (74%) AI deals being early-stage in 2024, investors are staking out early claims to reap the rewards of the tech’s potential.

Aside from AI, venture dealmaking is in a drought. Globally, deal activity fell 19% YoY to 27K in 2024 — its lowest annual level since 2016. The drop was most pronounced in countries like China (-33% YoY), Canada (-27%), and Germany (-23%). However, several countries in Asia — Japan, India, and South Korea — have bucked the downward trend. Their resilience suggests attractive investment conditions.

AI and industrial automation are common themes among the fastest-growing tech markets. Out of 1,400+ tech markets that CB Insights tracks, those with the highest rate of YoY deal growth include enterprise AI agents, genAI for customer support, industrial humanoid robots, and autonomous driving systems. Expect these technologies to continue maturing in 2025, increasing their disruptive potential.

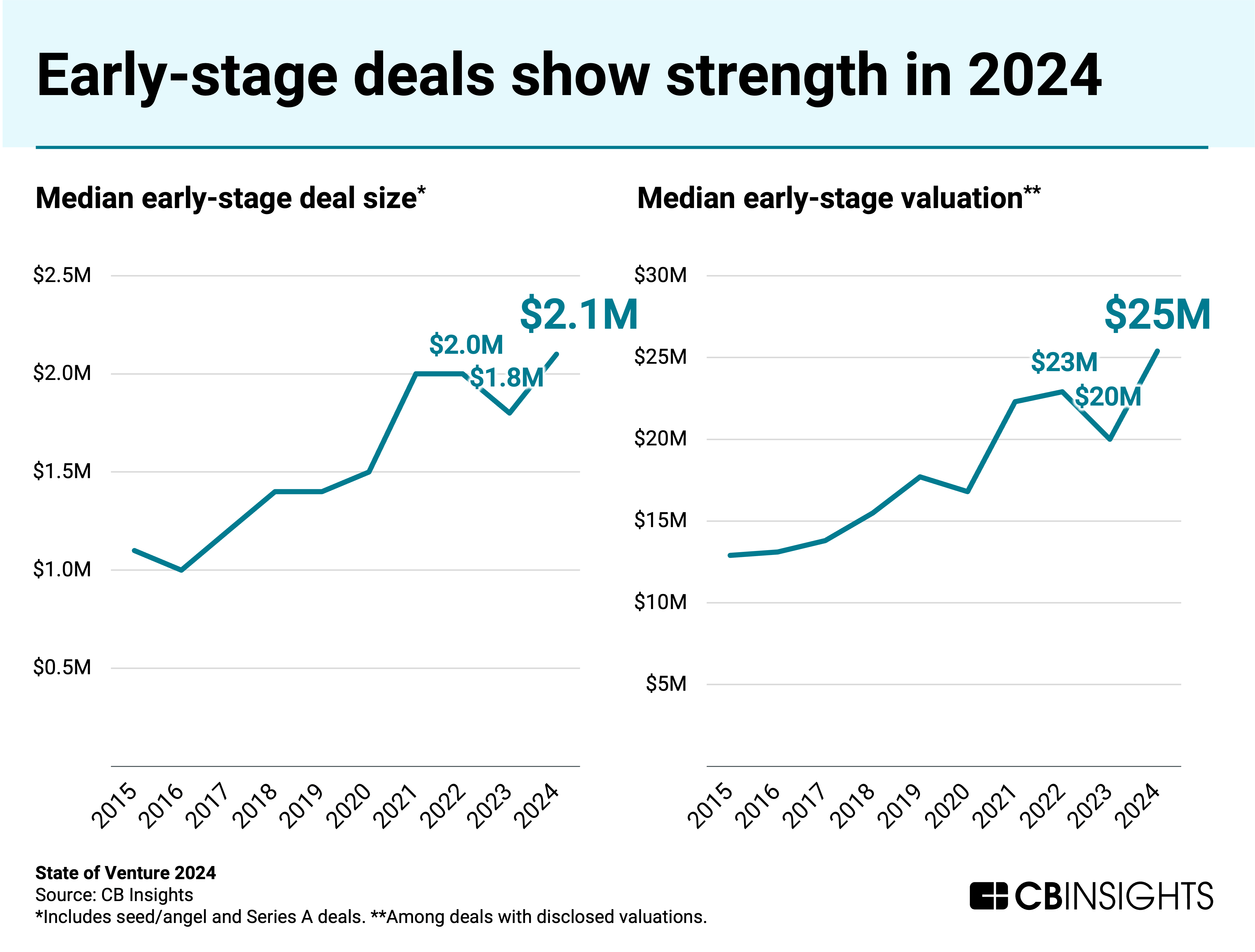

Despite market uncertainty, early-stage valuations hit a record-high median of $25M in 2024. Investors are packing into early-stage rounds to ride the next major wave of value creation in tech, likely drawn by startups’ ability to now build products with less capital and fewer people thanks to AI tools and infrastructure. However, early-stage startups could face a reality check when they try to raise later-stage rounds if they have yet to prove they can sustain growth. Although mid- and late-stage deal valuations rebounded slightly vs. 2023, they remain muted compared to 2021 and 2022.

IPO timelines get delayed. From first funding to IPO, VC-backed companies that went public in 2024 waited a median of 7.5 years — 2 years longer than in 2022. Amid unfavorable market conditions, some late-stage players like Stripe and Databricks have resorted to raising additional equity funding or selling private shares in lieu of going public. This allows them to create liquidity for early investors and employees when the path to a public debut is rocky.

We dive into each trend below.

AI is eating VC

The 5 largest deals of the year all went to AI model and infrastructure players (led by Databricks’ $10B Series J, followed by a $6.6B round for OpenAI, two $6B rounds for xAI, and a $4B round for Anthropic). But the activity isn’t limited to the largest, most well-resourced AI players.

Across the board, AI companies are capturing a higher share of deal volume — nearly one in 5 deals (17%) now go to AI companies, almost triple the share from 2015 (6%). AI deal volume remained above 4,000 for the fourth year in a row.

The boom is providing tailwinds for every stage of the startup lifecycle, from early-stage companies — which take 3 out of 4 deals in AI — to startup exits. The AI M&A wave is in full force, with 2024’s 384 exits nearly rivaling the previous year’s record-high 397.

This trend will continue in 2025 as incumbents look to grab AI tech and talent and build end-to-end AI offerings. Get the full breakdown of what AI M&A means for corporate strategy in our Tech Trends 2025 report.

In Q4’24, the AI boom helped fuel a substantial rebound in global funding. The quarter’s funding tally reached $86.2B — a 2-year high, and an increase of 53% quarter-over-quarter (QoQ).

60% of that quarterly total, or $52B, came from mega-rounds (deals worth $100M+) — nearly tying Q1’21 (61%) for the highest share ever across venture.

At the same time, quarterly deal volume steadily declined throughout 2024, including slipping below 6,000 in Q4’24 for the first time since 2016.

Aside from AI, venture dealmaking is in a drought

Global deal volume hits an 8-year low of 27K deals in 2024

{kind=link}

Despite AI’s surge, most venture sectors face their worst dealmaking drought in nearly a decade, forcing investors to adjust their strategies. Many investors are taking a more selective and risk-off approach right now as they wait out macroeconomic volatility and geopolitical tensions.

Among major dealmaking countries and regions (those seeing 500+ deals per year), the slump was most pronounced in China (-33% YoY drop in deals), Canada (-27%), and Germany (-23%).

However, several countries in Asia bucked the trend and notched slim YoY gains: Japan (+2%), India (+1%), and South Korea (+1%). These countries have invested heavily in developing their startup ecosystems and may be benefiting indirectly from investors diverting funds away from China.

AI and industrial automation are common themes among the fastest-growing tech markets

AI and industrial automation are at the center of some of the fastest-growing markets in tech.

We filtered CB Insights’ 1,400+ tech markets for those with at least 20 equity deals over the last 2 years, then singled out those with the strongest deal growth YoY in 2024.

The enterprise tech and industrials sectors dominate, comprising 9 of the top 10 tech markets. Advancements in generative AI are fueling much of the activity in areas like

humanoid robots and autonomous driving systems. Investors are also backing tech companies improving industrial processes like water treatment and purification, with deals to the market more than doubling YoY.

The enterprise tech and industrials sectors are also seeing a wave of hiring, as they lead in YoY headcount growth among all sectors. Industrials markets saw an average of 11% headcount growth last year, followed by enterprise tech markets with 10%.

Financial services and the consumer & retail industries are noticeably absent from the top 10 fastest-growing markets. Given the tough venture landscape, emerging technologies in these areas face an uphill battle.

Early-stage deals are showing strength

Globally, early-stage dealmaking represents one of the most vibrant areas of venture right now, with median deal size and valuation reaching all-time highs in 2024.

Early-stage deals show strength in 2024, with deal sizes and valuations reaching record highs

{kind=link}

The seed/angel and Series A stages remain resilient despite the broader downturn, in part because investors view them as a safe haven to ride out late-stage challenges like constricted exit opportunities and capital constraints. Deal sizes and valuations for the mid- and late stages rebounded slightly vs. 2023 but were muted when compared to the boom times of 2021 and 2022.

Corporate strategy and development teams seeking out early-stage opportunities can see 900+ high-potential startups here. To identify these players, we looked at the nearly 11,000 VC-backed startups that raised seed or Series A rounds in 2024, then filtered for those with the healthiest businesses (600+ Mosaic score) and strongest management teams (600+ Management Mosaic score).

IPO timelines get delayed

VC-backed startups wait a median of 7.5 years from first funding to IPO in 2024

{kind=link}

Most tech firms continue to shirk the IPO market. Some are still waiting for macroeconomic conditions to stabilize, while others prefer to focus on topline growth without having to deal with the financial scrutiny that comes with being a public company.

This is pushing back the timelines for IPO-ready companies even further.

From first funding to IPO, VC-backed companies that went public in 2024 waited a median of 7.5 years — 2 years longer than in 2022.

While Q4’24 saw an uptick in global IPOs, activity remains down vs. historical levels. In the current climate, many late-stage startups will likely opt instead to raise more private funding to sustain operations and pay out employees or early investors.

Related resources from CB Insights:

- Live briefing on venture trends for 2025

- All AI research from CBI

- 15 tech trends to watch closely in 2025

- Game Changers 2025: 9 technologies that will change the world

- $1B+ Market Map: The world’s 1,249 unicorn companies in one infographic

If you aren’t already a client, sign up for a free trial to learn more about our platform.